Bobby Darvish has been involved in the mortgage industry since 1998 He is a Certified Mortgage Planning Specialist from CMPS Institute, has studied residential mortgage & commercial mortgage underwriting courses, is a Business Finance Consultant graduate as well as a licensed broker.

Mortgage rates rose for the second week,

averaging 3.45 percent for a 30-year, fixed-rate loan, up from 3.42

percent the week before. A year ago, rates averaged 4.04 percent,

according to Freddie Mac’s weekly survey.

Despite the uptick, rates have held below 4

percent since December, tying a 29-week run of cheap borrowing we had

from November 2014 to June 2015.

During that sprint, the cost of a 30-year loan averaged 3.77 percent. This time, it’s held to 3.64 percent.

In a Redfin survey,

47 percent of all buyers said they’d look for a less expensive house if

rates rose by a point or more. Among respondents 34 and younger, the

share was more than 50 percent. Five percent of millennials said they’d

give up looking for a house altogether if rates jumped.

Source: Freddie Mac

Recommended by Forbes

Rates are lower now than they were in May, when the survey was taken. That’s one reason June was one of the most competitive months on record for home sales, according to Redfin data.

Mortgage rates will tick up and down week to week, but they’ll stay low for the foreseeable future.

“We don’t expect any significant movement

in mortgage rates in the near term,” Freddie Mac chief economist Sean

Becketti said. “This summer remains an auspicious time to buy a home or

to refinance an existing mortgage.”

The author is the professor of practice and senior director of the Oregon Economic Forum at the University of Oregon and the author of Tim Duy's Fed Watch.

The Federal Reserve eschews balance sheet policy – changes in the amount or composition of assets held by the central bank – in the early stages of itsplans to normalize the extraordinary monetary policy it instituted in the wake of the financial crisis. Instead, the Fed’s normalization plans currently focuses on raising the federal funds rate. But the central bank may need to use both rate policy and balance sheet policy simultaneously to reach the objectives of its dual mandate – or price stability with maximum sustainable employment – while sustaining a financial environment consistent with those objectives.

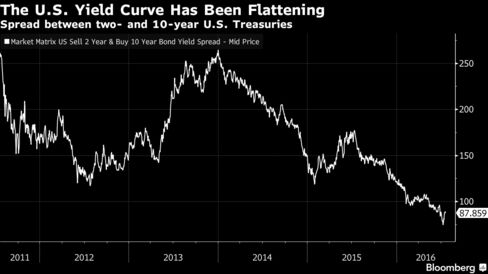

The flattening of the U.S. yield curve as investors see little chance of rates rising in the longer term should serve as a red flag that their focus on short-term interest rates may be doomed to failure.

Source: Bloomberg

One of the defining features of this tightening cycle is the same as the cycles that came before – the yield curve is flattening, and very quickly. The spread between 10-year and two-year U.S. Treasuries has collapsed to 88 basis points at a time when the federal funds target rate is 25-50bps. This suggests that the Fed actually has very little room to raise short-term rates. If additional rates hikes compress the yield curve further, the capacity for maturity transformation – effectively the process of borrowing on shorter time frames to lend on longer time frames – will soon be compromised.

Federal Reserve Governor Daniel Tarullo sees the threat. Speaking with the Wall Street Journal, he said:

Tarullo said he didn't think that the worry that low interest rates may fuel asset bubbles was an “immediate concern.”

The Fed governor, who is the quarterback of the Fed's efforts to regulate banks, questioned whether raising rates would ease financial stability concerns in an environment where the market was pessimistic about the economic outlook.

“If markets do regard economic prospects as only modest or moderate going forward, then raising short-term rates is almost surely going to flatten the yield curve, which generally speaking is not good for financial intermediation, and in some sense could exacerbate financial stability concerns,” Tarullo said.

When rates are low, regulators should pay more attention to financial stability issues "but it doesn't translate into 'therefore raise rates and all will be well,'" he added.

Some of Tarullo's colleagues at the Fed are pushing for rate hikes sooner rather than later on the basis of two economic narratives. The first essentially collapses to a Phillips curve story. In other words, as slack in the labor market decreases, inflationary pressures rise. To stem those pressures, the Fed needs to raise rates early, especially if they want to achieve a slow pace of subsequent rate hikes.

The problem with this story is that the Phillips curve is flat as a pancake, hence the calls for early rate hikes to quell inflationary pressures fall on some deaf ears around Constitution Avenue. This is especially the case after a long period of below target inflation and, perhaps more worrisome, evidence of declining inflation expectations. It is simply hard to build much support for the "we need to raise rates because of inflation" case in this environment.

In the absence of a strong inflation argument to justify rate hikes, some Fed policymakers are leaning more heavily on a second narrative, the financial stability angle — the fear that low rates foster asset bubbles or, perhaps worse, dangerously high levels of leverage within the financial sector.

For instance, San Francisco Federal Reserve President John Williams recently said:

"The risk I think we face in waiting too long, or waiting maybe as long as some of these market expectations are, is that the economy is already pretty strong and if we wait too long in further removal of accommodation I do think imbalances will form more generally. It could show up as more inflation pressures down the road, we're not seeing those yet, but I think that you do see some of this in terms of real-estate markets and other asset markets which are being priced to perfection based on an outlook of very low interest rates. You are seeing extremely high asset valuations in real estate, commercial real estate, the stock market is very strong relative to fundamentals. That is a natural result from low interest rates, that's one of the ways monetary policy affects the economy. But if asset prices, real estate prices, continue to go further and further away from longer-term fundamentals I think that creates risk for the economy, I think it creates risks eventually for the financial system."

Tarullo will likely push back against this line of thought. Raising interest rates alone may not alleviate financial stability concerns. In fact, they may aggravate those concerns if the yield curve continues to flatten. In contrast, consider the implications of a potential policy path charted in June of 2015 by New York Federal Reserve President William Dudley:

"An important aspect of current financial market conditions is the very low bond term premia around the globe. If a small rise in short-term rates were to lead to an abrupt increase in term premia and bond yields, resulting in a significant tightening in financial market conditions, then the Federal Reserve would likely move more slowly — all else equal. As an example, consider the experience of the 1994-95 tightening cycle. Bond yields rose sharply and the Federal Reserve tightened less than what was ultimately priced in by market participants. Conversely, if term premia and bond yields were to remain low and the economic outlook suggested that financial conditions needed to be tighter and a rise in short-term rates did not generate this outcome, then the FOMC would likely need to raise short-term rates further than anticipated. The 2004-2007 tightening cycle might be a good example of this. The FOMC ultimately pushed the federal funds rate up to a peak of 5.25 percent, in part, because the earlier rise in short-term rates was generally ineffective in tightening financial market conditions sufficiently over this period."

Dudley, at least last year, believed that during the 2004-2007 cycle the Fed needed to push harder on the short end of the curve because the long end wasn't responding. In the process, the Fed inverted the yield curve, which only exacerbated the financial crisis along the lines of Tarullo’s thinking. Policymakers need to think carefully before they create conditions that interfere with maturity transformation and hence financial intermediation. Following Dudley's 2015 advice now by raising short rates to quell nascent financial stability problems would be a complete disaster. He probably realizes this.

But note too that Dudley looks disapprovingly on the 1994-1995 cycle. For policymakers at the Fed, that cycle has left an indelible mark on their psyche. The just can't shake it. And 2013's "taper tantrum," or the steepening of the yield curve in the wake of former Federal Reserve Chair Ben Bernanke's hints that quantitative easing was ending, revived their fear of a 1994 repeat. The Fed doesn’t like a steep yield curve, but they won’t like a flat one either.

So what's a central bank to do? They try to exit this quandary through forward guidance — attempting to control the long-end of the curve by signaling their intentions for the short-end. This does not appear to be working; the interaction of policy and guidance are flattening the curve further but leaving short-term rates near zero. As it stands, it is all too easy to see the economy gaining sufficient momentum to prompt the Fed to tighten further, but that tightening would quickly invert the yield curve and send the credit creation process on a recessionary trajectory.

Tarullo provided another path for the Fed to follow in a 2014 speech:

"Finally, it may also be worth considering some refinements to our monetary policy tools. Central banks must always be cognizant of important changes that may result in different responses of households, firms, and financial markets to monetary policy actions. There is little doubt that the conduct of monetary policy has become a good deal more complicated in recent years. Some of these complications may diminish as economic and financial conditions normalize, but others may be more persistent. Central banks, in turn, may want to build on some recent experience, adapted for more normal times, in addressing the desire to contain systemic risk without removing monetary policy accommodation to advance one or both dual mandate goals. One example would be altering the composition of a central bank's balance sheet so as to add a second policy instrument to changes in the targeted interest rate. The central bank might under some conditions want to use a combination of the two instruments to respond to concurrent concerns about macroeconomic sluggishness and excessive maturity transformation by lowering the target (short-term) interest rate and simultaneously flattening the yield curve through swapping shorter duration assets for longer-term ones."

In this example, he suggests responding to financial market excess in a weak economy by flattening the curve via balance sheet tools while lowering rates. The lesson, however, is more general. The Fed needs to think of policy in terms of using two tools — rates and balance sheet — simultaneously. Forward guidance alone might not be sufficient to allow the rate tool to mimic the impact of both jointly. In the current environment, should the Fed want to increase rates to tighten policy but at the same time be concerned about excessive flattening of the yield curve, they would need to sell long-dated Treasuries from their portfolio to normalize policy. Depending on conditions, this may be in concert with rate hikes at the short-end.

In effect, the Fed should consider the need for two targets, both the level of rates and the slope of the yield curve, as essential for meeting their policy goals. For now, the Fed appears committed to just the interest rate tool. And in some ways, that is no surprise. Short-term rates are a comfortable tool for the Fed, whereas playing with the yield curve via the balance sheet is seen as fraught with danger. But with the yield curve flattening as the economy approaches full employment, they may find themselves unable to maintain the appropriate level of financial accommodation via rate policy alone.

Bottom Line: The Fed needs to remember that how they got into this policy stance may offer a lesson for how to get out. Policy makers cut rates to zero and then instituted quantitative easing. Now they should consider selling assets before raising rates. Or, at a minimum, utilizing a mixed strategy of rate hikes and asset sales. The objective of meeting the Fed's mandate in the context of maintaining financial stability may be unattainable using the interest rate tool and associated forward guidance alone. Unfortunately, the Fed does not appear to be debating the policy mix — at least not in public. They remain focused on interest rates, delaying balance sheet policy to a later date. On the current trajectory, however, that later date may never come.

For all your mortgage needs you can reach Bobby Darvish of Platinum Lending Solutions.

Record low mortgage interest rates mean big savings for home buyers and those refinancing a mortgage.

In January I thought I had written my last column about record-low

interest rates, and just how much they can benefit home buyers and

mortgage refinancers.

Like many people who figured interest rates had nowhere left to go but up, I was mistaken.

Borrowing $200,000 today for a 30-year mortgage would cost about $850 a

year less, in annual payments, than borrowing that same amount in

December. To put it another way, the payments on a $210,000 loan at

today’s rates would be the same as the payments on a $200,000 loan

secured in December.

For homeowners who already have mortgages, rising real estate values

have been increasing the amount of equity those homeowners have, making

it possible for more people to refinance. Owners who were “underwater”

on their loans previously may now have a chance to jump to a lower

interest rate. (Equity is what the property is worth, minus the

outstanding debt. When the debt’s larger than the equity a loan is

underwater).

Consider that a $200,000 mortgage loan, today, would cost $2,700 less

each year than borrowing the same amount 10 years ago, during the height

of the housing price bubble. The going interest rate was 5.62 during

the first week of July, 2006, according to the feds who track such

things.

Mortgage interest rates have now fallen to all-time lows. There are

many reasons why, but the short and oversimplified version is, investors

have been buying U.S. Treasury bonds as a safe haven during uncertain

times — slow U.S. economic growth, negative interest rates overseas, the

“Brexit” and other factors — and that pushes interest rates down.

These low interest rates will give home buyers one more opportunity to

lock in long-term loan rates that are lower than they have ever been.

They will give people with existing loans one more chance to refinance

to record-low rates.

How low are we talking about? For people with good to excellent

credit, 740 or better, a 30-year mortgage could be had this week at a

fixed interest rate of 3.375 percent. A 15-year mortgage could be had

for 2.75 percent, according to the folks at Lucey Mortgage in Mount

Pleasant (disclosure: they handled my mortgage refinance last month).

Potential home-buyers in South Carolina should also remember to inquire about getting a mortgage credit certificate.

For those who qualify, obtaining a mortgage credit certificate from a

lender before closing on a home purchase entitles the holder to an

annual federal tax credit worth up to $2,000.

For those considering refinancing, here are a few important points to remember.

The decision to refinance depends on

balancing the up-front costs against the expected savings, which will

vary depending on the interest rate, the loan term, the closing costs,

and how long the borrower expects to stay in the house. It’s easy to go

online and see not only what the loan payment would be on a mortgage,

but also how a refinance could help build equity more quickly (search

online for “mortgage amortization calculation” — bankrate.com has a good

one).

There are costs involved with refinancing,

such as title research, an appraisal, a lawyer to review closing

documents, and lender fees. Costs can vary widely, so compare closing

costs as well as interest rates. When I shopped for my recent

refinancing, I found costs that varied by as much as $1,500.

Refinancing can leave you with a longer

mortgage, or a shorter one. Common terms are 30 or 15 years, but 20

years is also an option. Shorter-term loans build equity faster and have

lower interest rates, but have higher monthly payments. The lowest

payments come with 30-year loans, but most of the money goes towards

interest in the early years.

Don’t overlook the fine print. Make sure a loan allows you to pay it off at any time, with no penalty, for example.

I won’t guess what the future holds, in terms of interest rates or the

real estate market. What I know is that mortgage interest rates have

never been lower. There may not be a better time to refinance, but if

there is, I’ll write about it.

The Brexit aftermath has rattled the stock market and led to decline in

mortgage rates. While lower mortgage rates have been affecting

retirement accounts, they are helping people seeking to refinance their

home loans.

Notably, in the last week of June, the 30-year

fixed-rate mortgage averaged 3.48%, down from 3.56% in the prior week.

The 15-year fixed-rate mortgage averaged 2.78%, down 5 basis points

(bps). Further, the 5-year Treasury-indexed hybrid adjustable-rate

mortgage averaged 2.70%, declining from 2.74%.

Following Brexit,

the 10-year U.S. Treasury yield, which serves as benchmark for consumer

loans, tumbled 24 bps to 1.45%. Sean Becketti, Freddie Mac chief

economist stated, "This week's survey rate is the lowest since May 2013

and only 17 basis points above the all-time low recorded in November

2012. This extremely low mortgage rate should support solid home sales

and refinancing volume this summer."

Mortgage rates are

correlated to the 10-year U.S. government bonds yield. In Dec 2015, the

Federal Reserve announced the most awaited increase in the benchmark

federal funds rate after more than nine years and had plans to announce

four more hikes in 2016. This, in turn, led 10-year Treasury yields to

rise followed by mortgage rates.

However, no further hike has

been announced by the Fed so far, as it is reconsidering its plans in

the wake of the uncertainty prevailing in the global financial market.

In June meeting, the rate hike decision was kept on hold as “A U.K. vote

to exit the European Union could have significant economic

repercussions,” Fed Chair Janet L. Yellen stated. As a result, yields on

10-year Treasury notes plummeted to low levels since 2012.

Moreover,

Brexit gave rise to anxiety among investors, compelling them to seek a

safe refuge. All this ultimately led to ultra-low mortgage rates which

are expected to go down further.

Low mortgage rates can be a boon

for the U.S. real estate market. The reduction in home loan rates is

expected to give the U.S. buyers some respite.

Though stock

prices in the U.S. have bounced back, Brexit impact is expected to stay

for a while – which might deal another blow to mortgage rates.

Meanwhile, this can perk up housing demand in July, supporting the

recovery in the economy.

In spite of the plunge in rates,

investors are apprehensive about investing in the housing market, thanks

to the volatility rippling through the financial world. However,

homeowners seeking lower rates for refinancing are definitely big-time

gainers.

"In light of the Brexit vote and other recent economic

news, MBA now predicts that the Fed will hike only once this year,

likely in December," said Lynn Fisher, Mortgage Bankers Association vice

president of research and economics. "If the financial-market

disruption from Brexit persists, the likelihood of even a December hike

would be reduced" he added. Therefore, such prediction is an added

advantage for both buyers and homeowners looking for financial aid at

lower rates.

Notably, low rates are expected to spur higher real

estate activity and lending as experienced in 2012. Therefore, for

mortgage lenders including Bank of America Corporation (BAC - Analyst Report) and Wells Fargo & Company (WFC - Analyst Report) , low rates could benefit their consumer and home loan businesses.

Though

low rates are a boon for homeowners, mortgage REITs might suffer. When

homeowners prepay, investors are forced to reinvest the proceeds in a

lower-rate investment yielding low returns. Therefore, rise in

prepayments turn out to be negative for REITs, including those with huge

exposure to fixed-rate, government-guaranteed mortgages. Such companies

include American Capital Agency (AGNC - Analyst Report) and Annaly Capital Management (NLY - Analyst Report) .